People who rent face impossible financial challenge in retirement

Need to know

- Everyone deserves a comfortable retirement, but people who rent are being left behind.

- To have the same standard of living as a person who owns their home in retirement, the typical person who rents would need around twice as much super.

- Unless this gap is filled by the Government providing more support, people who rent in retirement will struggle for decades in retirement.

Retirement savings targets for homeowners provide a rule of thumb to understand how much a typical retiree spends, and how much super you need to support that standard of living.

For the first time, we’ve also calculated spending levels and savings targets for retirees who rent. This new research shows the savings gap for renters and how much extra people who rent may need to maintain the same quality of life as someone who owns their home.

A typical single retiree who rents would need $659,000 in super compared to $322,000 in super needed by a retiree who owns their home. A couple who rents needs $786,000 combined in super compared to $432,000 combined in super for a couple who owns their home.

Spending for a decent standard of living

To figure out how much a retired person who is renting needs to spend to have a dignified retirement, we first looked at what renters actually spent and their level of financial satisfaction and stress. It wasn’t a pretty picture. The spending figures were so low that almost half of retired renters were in financial stress.

We wanted to give people targets that would mean they’d have a quality standard of living. So we used the low, medium and high amounts that homeowners spend. We swapped out what homeowners spend on their house (e.g. maintenance, etc) with rental costs for renters.

To keep things simple we assume single people rent one-bedroom apartments, and couples rent either a one-bedroom or two-bedroom apartments in capital cities. The typical one-bedroom rent across all capital cities averaged $470 per week in June 2025, with Sydney being the highest at $560 a week. In general Sydney and Canberra have higher rents than the average.

Rent data is sourced from the 2021 Census updated to June 2025 using the ABS rent CPI. We used the distribution of rents for one bedroom apartments for singles, and the distribution of rents across one bedroom and two bedroom apartments for couples. Low / Medium / High rents are the bottom quarter, middle quarter and top quarter of rents that people pay.

Accessible version

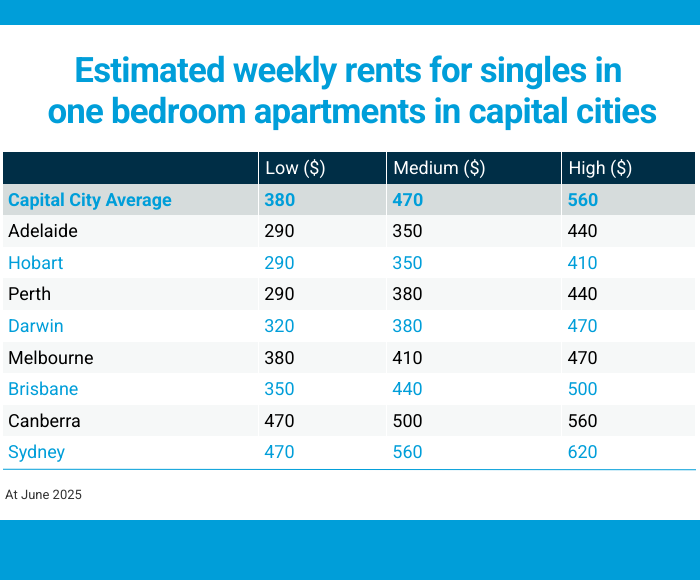

Estimated weekly rents for singles in one bedroom apartments in capital cities at June 2025

Average rent across all capital cities: low $380 per week, medium $470 per week, high $560 per week.

Rents in each capital city, ordered on medium weekly rents from cheapest city to most expensive city

Adelaide: low $290 per week, medium $350 per week, high $440 per week

Hobart: low $290 per week, medium $350 per week, high $410 per week

Perth: low $290 per week, medium $380 per week, high $440 per week

Darwin: low $320 per week, medium $380 per week, high $470 per week

Melbourne: low $380 per week, medium $410 per week, high $470 per week

Brisbane: low $350 per week, medium $440 per week, high $500 per week

Canberra: low $470 per week, medium $500 per week, high $560 per week

Sydney: low $470 per week, medium $560 per week, high $620 per week

Rent data is sourced from the 2021 Census updated to June 2025 using the ABS rent CPI. We used the distribution of rents for one bedroom apartments for singles, and the distribution of rents across one bedroom and two bedroom apartments for couples. Low / Medium / High rents are the bottom quarter, middle quarter and top quarter of rents that people pay.

Rent data is sourced from the 2021 Census updated to June 2025 using the ABS rent CPI. We used the distribution of rents for one bedroom apartments for singles, and the distribution of rents across one bedroom and two bedroom apartments for couples. Low / Medium / High rents are the bottom quarter, middle quarter and top quarter of rents that people pay.

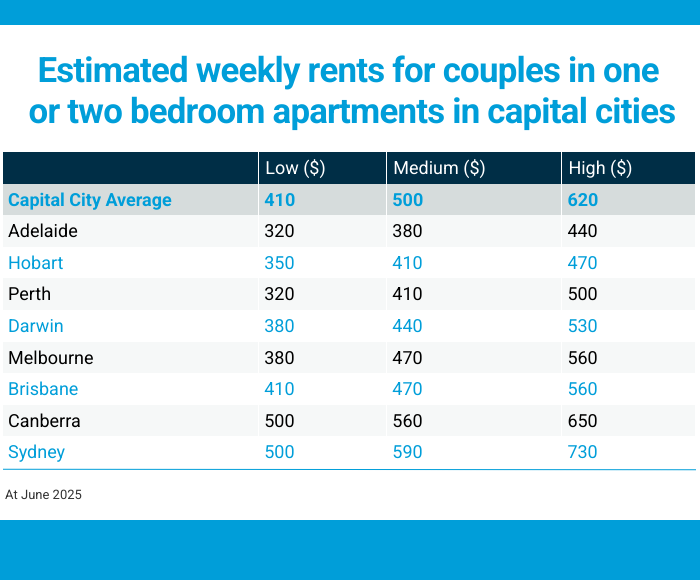

Accessible version

Estimated weekly rents for couples in one or two bedroom apartments in capital cities at June 2025

Average rent across all capital cities: low $410 per week, medium $500 per week, high $620 per week.

Rents in each capital city, ordered on medium weekly rents from cheapest city to most expensive city

Adelaide: low $320 per week, medium $380 per week, high $440 per week

Hobart: low $350 per week, medium $410 per week, high $470 per week

Perth: low $320 per week, medium $410 per week, high $500 per week

Darwin: low $380 per week, medium $440 per week, high $530 per week

Melbourne: low $380 per week, medium $470 per week, high $560 per week

Brisbane: low $410 per week, medium $470 per week, high $560 per week

Canberra: low $500 per week, medium $560 per week, high $650 per week

Sydney: low $500 per week, medium $590 per week, high $730 per week

Rent data is sourced from the 2021 Census updated to June 2025 using the ABS rent CPI. We used the distribution of rents for one bedroom apartments for singles, and the distribution of rents across one bedroom and two bedroom apartments for couples. Low / Medium / High rents are the bottom quarter, middle quarter and top quarter of rents that people pay.

2026 Retirement Savings Targets for Renters

The 2026 retirement savings targets for renters show how much super you’ll need to sustain your desired standard of living until age 90.

Accessible version

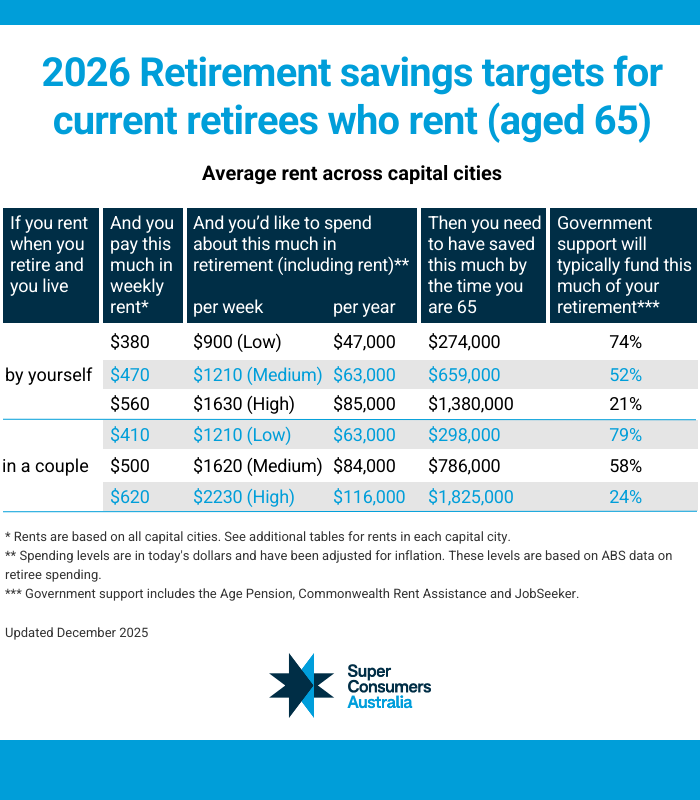

2026 Retirement savings targets for current retirees who rent (aged 65)

Using average rent across all capital cities, one bedroom apartments for singles and one or two bedroom apartments for couples

If you rent when you retire and you live by yourself…

Low

If you pay this much in rent per week: $380

Amount you wish to spend in retirement per week including rent: $900

Amount you wish to spend in retirement per year including rent: $47,000

You need to save this much in superannuation by age 65: $274,000

Government support would typically fund this much of your spending: 74%

Medium

If you pay this much in rent per week: $470

Amount you wish to spend in retirement per week including rent: $1210

Amount you wish to spend in retirement per year including rent: $63,000

You need to save this much in superannuation by age 65: $659,000

Government support would typically fund this much of your spending: 52%

High

If you pay this much in rent per week: $560

Amount you wish to spend in retirement per week including rent: $1630

Amount you wish to spend in retirement per year including rent: $85,000

You need to save this much in superannuation by age 65: $1,380,000

Government support would typically fund this much of your spending: 21%

If you rent when you retire and you live in a couple…

Low

If you pay this much in rent per week: $410

Combined amount you wish to spend as a couple in retirement per week including rent: $1210

Combined amount you wish to spend as a couple in retirement per year including rent: $63,000

Together you need combined savings in superannuation by age 65 of: $298,000

Government support would typically fund this much of your spending: 79%

Medium

If you pay this much in rent per week: $500

Combined amount you wish to spend as a couple in retirement per week including rent: $1620

Combined amount you wish to spend as a couple in retirement per year including rent: $84,000

Together you need combined savings in superannuation by age 65 of: $786,000

Government support would typically fund this much of your spending: 58%

High

If you pay this much in rent per week: $620

Combined amount you wish to spend as a couple in retirement per week including rent: $2230

Combined amount you wish to spend as a couple in retirement per year including rent: $116,000

Together you need combined savings in superannuation by age 65 of: $1,825,000

Government support would typically fund this much of your spending: 24%

Table notes:

Rents are based on averages across all capital cities. See additional tables for rents by capital city. Figures for couples represent the combined spending of two people living together. Spending levels are in today’s dollars and have been adjusted for inflation. These levels are based on ABS data about retirees’ spending. Government support includes the Age Pension, Commonwealth Rent Assistance and Jobseeker. Updated December 2025.

Across Australia, a typical single or couple who rents needs around twice as much super as homeowners to enjoy the same standard of living.

What does low, medium and high spending mean?

The low, medium and high spending levels provide a rule of thumb to help you figure out your spending needs.

High spending means a quarter of properties are more expensive than this to rent, and in addition to rent, your other spending is the same as high spending for homeowners (excluding their spending on housing).

To calculate spending for renters we used the low, medium and high amounts that homeowners spend, but swapped out their spending on housing with low, medium and high rents.

Low spending means a quarter of properties are cheaper than this to rent and in addition to rent, your other spending is the same as low spending for homeowners (excluding their spending on housing).

Medium spending means half of properties are cheaper and half are more expensive to rent, and in addition to rent, your other spending is the same as medium spending for homeowners (excluding their spending on housing).

Rents vary across capital cities, so we have calculated retirement spending and savings targets for renters in each capital city. In the cheapest cities to rent, retirees still need more than one and a half times as much superannuation than retirees who own their home.

Accessible version

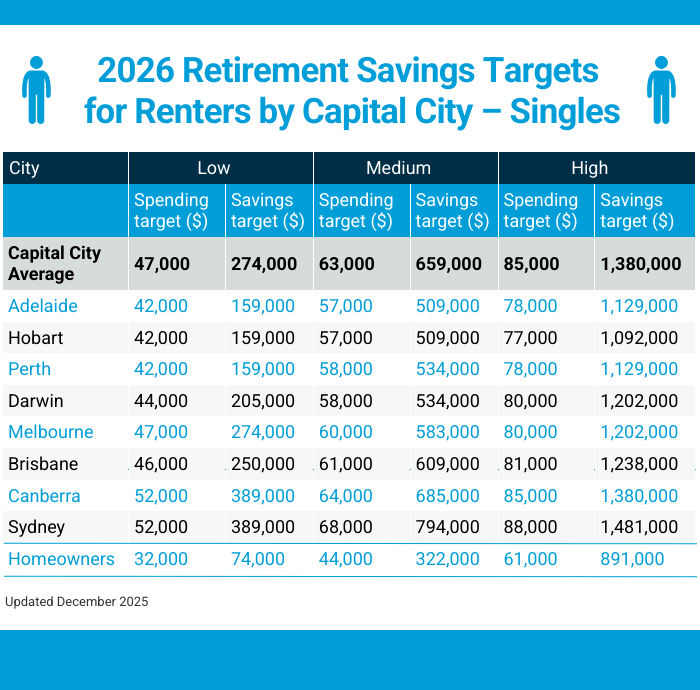

2026 retirement savings targets for renters by capital city for singles

Cities are ordered from lowest to highest medium spending level

Average across all capital cities:

For a low spending target of $47,000 per year the superannuation savings target is $274,000. For a medium spending target of $63,000 per year the superannuation savings target is $659,000. For a high spending target of $85,000 per year the superannuation savings target is $1,380,000.

In Adelaide:

For a low spending target of $42,000 per year the superannuation savings target is $159,000. For a medium spending target of $57,000 per year the superannuation savings target is $509,000. For a high spending target of $78,000 per year the superannuation savings target is $1,129,000.

In Hobart:

For a low spending target of $42,000 per year the superannuation savings target is $159,000. For a medium spending target of $57,000 per year the superannuation savings target is $509,000. For a high spending target of $77,000 per year the superannuation savings target is $1,092,000.

In Perth:

For a low spending target of $42,000 per year the superannuation savings target is $159,000. For a medium spending target of $58,000 per year the superannuation savings target is $534,000. For a high spending target of $78,000 per year the superannuation savings target is $1,129,000.

In Darwin:

For a low spending target of $44,000 per year the superannuation savings target is $205,000. For a medium spending target of $58,000 per year the superannuation savings target is $534,000. For a high spending target of $80,000 per year the superannuation savings target is $1,202,000.

In Melbourne:

For a low spending target of $47,000 per year the superannuation savings target is $274,000. For a medium spending target of $60,000 per year the superannuation savings target is $583,000. For a high spending target of $80,000 per year the superannuation savings target is $1,202,000.

In Brisbane:

For a low spending target of $46,000 per year the superannuation savings target is $250,000. For a medium spending target of $61,000 per year the superannuation savings target is $609,000. For a high spending target of $81,000 per year the superannuation savings target is $1,238,000.

In Canberra:

For a low spending target of $52,000 per year the superannuation savings target is $389,000. For a medium spending target of $64,000 per year the superannuation savings target is $685,000. For a high spending target of $85,000 per year the superannuation savings target is $1,380,000.

In Sydney:

For a low spending target of $52,000 per year the superannuation savings target is $389,000. For a medium spending target of $68,000 per year the superannuation savings target is $794,000. For a high spending target of $88,000 per year the superannuation savings target is $1,481,000.

By comparison, for people who own their home:

The low spending target is $32,000 per year and the superannuation savings target is $74,000. The medium spending target is $44,000 per year and the superannuation savings target is $322,000. The high spending target is $61,000 per year and the superannuation savings target is $891,000.

Table note: Updated December 2025

Accessible version

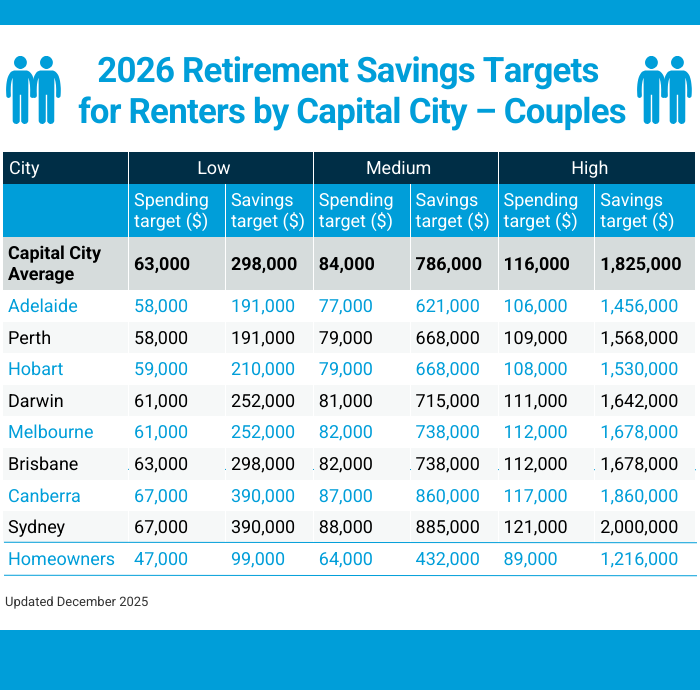

2026 retirement savings targets for renters by capital city for couples

Cities are ordered from lowest to highest medium spending level

Amounts are combined spending and savings of two people living together.

Average across all capital cities:

For a low spending target of $63,000 per year the superannuation savings target is $298,000. For a medium spending target of $84,000 per year the superannuation savings target is $786,000. For a high spending target of $116,000 per year the superannuation savings target is $1,825,000.

In Adelaide:

For a low spending target of $58,000 per year the superannuation savings target is $191,000. For a medium spending target of $77,000 per year the superannuation savings target is $621,000. For a high spending target of $106,000 per year the superannuation savings target is $1,456,000.

In Perth:

For a low spending target of $58,000 per year the superannuation savings target is $191,000. For a medium spending target of $79,000 per year the superannuation savings target is $668,000. For a high spending target of $109,000 per year the superannuation savings target is $1,568,000.

In Hobart:

For a low spending target of $59,000 per year the superannuation savings target is $210,000. For a medium spending target of $79,000 per year the superannuation savings target is $668,000. For a high spending target of $108,000 per year the superannuation savings target is $1,530,000.

In Darwin:

For a low spending target of $61,000 per year the superannuation savings target is $252,000. For a medium spending target of $81,000 per year the superannuation savings target is $715,000. For a high spending target of $111,000 per year the superannuation savings target is $1,642,000.

In Melbourne:

For a low spending target of $61,000 per year the superannuation savings target is $252,000. For a medium spending target of $82,000 per year the superannuation savings target is $738,000. For a high spending target of $112,000 per year the superannuation savings target is $1,678,000.

In Brisbane:

For a low spending target of $63,000 per year the superannuation savings target is $298,000. For a medium spending target of $82,000 per year the superannuation savings target is $738,000. For a high spending target of $112,000 per year the superannuation savings target is $1,678,000.

In Canberra:

For a low spending target of $67,000 per year the superannuation savings target is $390,000. For a medium spending target of $87,000 per year the superannuation savings target is $860,000. For a high spending target of $117,000 per year the superannuation savings target is $1,860,000.

In Sydney:

For a low spending target of $67,000 per year the superannuation savings target is $390,000. For a medium spending target of $88,000 per year the superannuation savings target is $885,000. For a high spending target of $121,000 per year the superannuation savings target is $2,000,000.

By comparison, for couples who own their home:

The low spending target is $47,000 per year and the superannuation savings target is $99,000. The medium spending target is $64,000 per year and the superannuation savings target is $432,000. The high spending target is $89,000 per year and the superannuation savings target is $1,216,000.

Table note: Updated December 2025

What we found

- The high cost of rent actually means people who rent in retirement need to spend 30 to 47% more than homeowners to have the same standard of living.

- Across Australia, renters need one and a half to three times as much super as homeowners to enjoy the same standard of living.

- Commonwealth Rent Assistance does not come close to covering the rental costs for people living in capital cities.

- For a single person, rent assistance is $5,600.40 per year, but we know that rent is typically $19,700 or more per year.

- It isn’t keeping up. Commonwealth Rent Assistance increased by only 2% from September 2024 to September 2025, while rents rose 4.5% in the same period.

The high cost of rent actually means people who rent in retirement need to spend 30 to 47% more than homeowners to have the same standard of living.

How we calculated the figures

Spending

We use the housing and non-housing spending of homeowners from the ABS Household Expenditure Survey, and adjust these amounts to today’s dollars by using the ABS Household Expenditure data from the latest National Accounts to incorporate a change to the bundle of goods that households are spending on, and using the ABS Age Pensioner Living Cost Index to adjust for changes in prices.

For retirees who rent we use the non-housing spending of retirees who own their home so both groups have the same quality of life.

To figure out the amount of rent we follow the methodology used by the Grattan Institute, updated to June 2025 using the ABS rent CPI. We use rents for 1-bedroom apartments in major capital cities for single retirees and rents in 1- or 2-bedroom apartments in major capital cities for couple retirees.(see Grattan Institute report “Renting in Retirement” figure 1.8, page 15).

We focused on rents for apartments in capital cities as 73% of people in Australia live in major cities. (see AIHW, Profile of Australian Population).

Superannuation savings target

The savings targets provide the amount a person needs to have saved in superannuation by age 65 in order to spend at the income level stated until age 90.

We assume a person starts retirement at age 65. According to the ABS, the average age of people who retired in 2024-25 was 63.8 years. (see ABS Retirement and Retirement Intentions statistics).

To produce the targets, we use a model that incorporates the ups and downs of investment returns over time. Our savings targets provide 90% confidence that, even given uncertain investment outcomes in retirement, spending is sustained to age 90.

We assume that income comes from spending some superannuation balance each year, plus government payments that a person would be entitled to, based on the superannuation balance and assuming $25,000 in other assets.

In addition to the Age Pension, we include the Commonwealth Rent Assistance payment as at September 2025 of $215.40 per fortnight for singles and $203 per fortnight for couples.

To ensure a person who is renting and retires at age 65 can access Commonwealth Rent Assistance, we assume that this person will access unemployment payments (JobSeeker) for two years before becoming eligible for the Age Pension at age 67.

Unemployment payments are available to people over age 60 who can meet the ‘mutual obligations requirements’, which includes volunteering for 30 hours a fortnight. Those unable to volunteer for 30 hours a fortnight due to disability, may be eligible for the Disability Support Pension, which has higher payments than unemployment benefits.

Renters face growing pressure

Retired renters continue to face higher rates of financial stress and poverty than homeowners.

Government data from the Australian Institute of Health and Welfare shows there were over 325,000 Age Pensioners receiving Commonwealth Rent Assistance in June 2025, and 32% (105,000) were still in rental stress (spending more than 33% of their income on rent) after receiving Commonwealth Rent Assistance.

In June 2025, 105,000 Age Pensioners were still in rental stress (spending more than 33% of their income on rent) after receiving Commonwealth Rent Assistance.

Our new analysis confirms that renters need significantly more savings to achieve the same quality of life — yet Commonwealth Rent Assistance isn’t keeping pace with rising costs.

“We need systemic change, not just advice to save more,” says Super Consumers Australia CEO Xavier O’Halloran.

“The government must increase Commonwealth Rent Assistance, link it to rent CPI, and invest in housing designed for older Australians.”

Super Consumers is not alone in calling for changes to ensure people who rent in retirement are not left behind.

The Australian retirement system is built on the expectation that older people will own a home at the time of retirement, however, there has been a 73% increase over ten years in the number of older renters. Living in expensive and poor quality homes is impacting the health and wellbeing of older renters, and preventing their ability to age well and with dignity.

We need to address this retirement divide, by building more public and community housing, reforming housing-related tax concessions, cap rent increases to no more than CPI, and raising the rate of income support payments.

Fiona York, CEO of advocacy group Housing for the Aged Action Group, Inc

People with low incomes who rent are struggling to keep a roof over their heads. The solution does not lie with superannuation. To prevent homelessness and ensure that everyone who is renting can afford a decent home, the government should urgently do three things:

- Increase the lowest income support payments such as Jobseeker and Youth Allowance to at least $589 per week;

- Lift maximum rates of Rent Assistance substantially so they are in touch with the cost of renting today;

- Set and fund a target to increase social housing nationally to at least its historical level of 6% of homes within a decade and 10% of homes in two decades to alleviate housing stress of people on low incomes

Australian Council of Social Service

Where to get help

For free and independent information:

- Visit moneysmart.gov.au or the Financial Information Service

If you’re struggling with debt, contact the National Debt Helpline on 1800 007 007

The development and ongoing maintenance of our retirement targets is supported by a philanthropic grant from Ecstra Foundation, which is committed to building the financial wellbeing of Australians within a fair financial system.