I signed up for a ‘super health check’. What I got was an $11,000 bill.

Social media platforms have been a boon for anyone looking to get a product in front of a consumer.

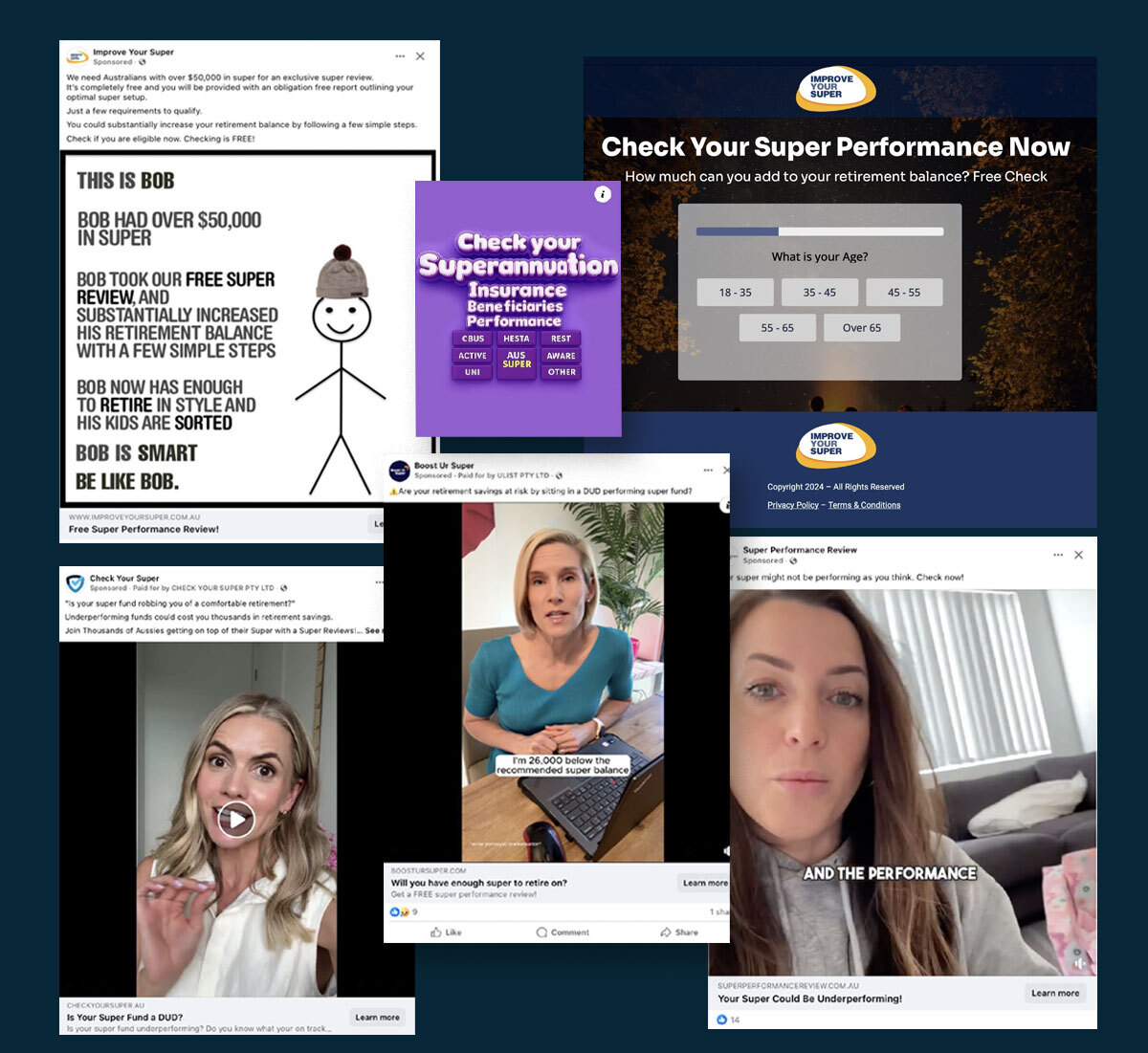

The plight of the snake oil salesman used to be a hard one. You’d have to go town to town selling your half truths and lies, hoping no one from the town you just left caught up with you. Social media platforms solved this problem, they let the modern snake oil salesman reach everyone with a device in seconds. The platforms have done little to protect consumers in the process. They’ve got no incentive to: the shonks are among the social media platforms’ best paying customers. With social media, these salesmen can sell at scale in record time leaving regulators, honest market participants and consumers to pick up the pieces.

This is the story of high risk super switching, the practice that has already ripped over a billion dollars from people looking to save for their retirement after people were funneled on an industrial scale into two dodgy investments. Yet these business models survive and cause catastrophic harm to people. They will do far worse if we don’t stop them.

My job is superannuation. I’d seen the consumer awareness campaigns warning people off high risk super switching and heard the catch cries, ‘if it sounds too good to be true it probably is’. I decided to sign up for one myself.

It was easy enough. My instagram feed was overflowing with advertisements showing ordinary people living busy lives who knew they should be paying more attention to their super, but didn’t know where to start. It was relatable, common sense guidance. They told me the government had tested the performance of funds and with a simple ‘super health check’ I could find out if I was in one of the ones that failed. I entered my contact details and waited for a call.

A few days later, I got a call offering to put me in touch with a financial expert with over a decade of experience in super. The man I spoke to seemed knowledgeable, he was likable and complimented me for getting on top of my super at a young age. He even complimented me on the decisions I’d made to date, like taking on more risk for longer term returns. All the while he was running down the trust in my current super fund. He showed me how opaque their fee disclosures are, talked about super fund customer service failures and why my fund’s investment strategies deliver such poor returns. All good lies have an element of truth.

A week later I talked to a second financial adviser and was given a statement of advice with recommendations on what to do with my super. For someone with some knowledge of investment returns, there was no real magic to it. They recommended 16 exchange traded funds (ETFs). The key selling point of this type of investment is it is usually a relatively cheap way to own a diverse mix of investments. They looked like they had a stronger history of performance than my existing super fund. My fund was delivering 11.5% p.a. compared to almost 16% p.a. in the adviser recommended ETFs over the last 5 years. Looking under the hood, this 5-year comparison period was critical: most credible financial advice would use a longer timeframe among other types of comparisons. The last 5 years has been a boom period for semiconductors and gold. Lo and behold, the advice I received recommended ETFs that were heavily invested in these two markets.

Picking yesterday’s winners is not a skill. Semiconductors and gold may continue on their bull run for a while yet (although the glimmer has come off gold this year), but outperformance like this requires active management. Outside of an annual review, this is not what the financial adviser was offering. Conversely, my existing fund does actively manage my investments, so despite the sales pitch I likely would be much better off staying put.

All up, the advice was going to set me back $11,000 upfront and an ongoing advice fee of $3,800 a year. This is steep given the advice was relatively simple. In fact, it was cookie cutter. And much higher than the typical cost of advice, which is currently $4,700 according to the Financial Advice Association of Australia. On top of that, the administration and investment fees were 24% higher per year on the platform they recommended I join.

But here’s the thing. Even though I knew it was a switching scheme and I knew the advice was bad, it was still a very convincing sales pitch. They were smooth, they were professional and they took their time trying to convince me. I didn’t switch, but if I weren’t working in super… I might have.

I’m sharing this as a warning to consumers, but also as a call to action for the government. Australians have diligently saved to create a $4 trillion dollar superannuation system. It’s now time to protect it by banning these dodgy advertisers. We need consumer protections to make sure super platforms are responsible for keeping people safe. Charging someone $11,000 for cookie cutter advice should never be allowed. We know from the regulator that these platforms have been asleep at the wheel and we’ve heard reports of people being stung for $20,000 or more for dodgy switching advice. The bleeding of Australians’ retirement savings from inappropriate advice needs to end.

If my story sounds familiar, please check on your super and read about what you can do on the takeyoursuperback.com website. It was developed by Super Consumers Australia with the support of the Australian Securities and Investments Commission; it offers free, independent information to those impacted by the Shield and First Guardian Master Fund collapses.